The debt based monetary system has become quite extreme. On one hand, the US crossed the $35 trillion national debt milestone, placing a $104k burden on every US citizen. On the other hand, the Congressional Budget Office (CBO) puts federal expenditures for 2024 at 24.2% of GDP.

This divergence between profligate spending and debt ballooning puts the economy on a narrow path. It is exceedingly unlikely that USG would opt to reduce spending, most of which goes to social programs, entitlements and the military. The latter alone is the key ingredient that backs USD as world currency.

Conversely, this entails another Fed balance sheet expansion, with three 0.25% rate cuts this year already priced in. In turn, non-currency assets like equities, gold and Bitcoin are poised for growth yet again. At the root of this dynamic is the question of information validity.

Just as the US Bureau of Labor Statistics is expected to revise down job figures by up to one million between April 2023 and March 2024, the information corruption is visible with central banking itself. If the Federal Reserve can increase M2 money supply by 27% in 2020-21, the money itself loses informational coherence.

It is this why investors then seek equities, gold and Bitcoin. These assets become vehicles of value because currency loses its ability to reliably relay value. The problem is, they are also taxed as a way to subdue the velocity of exiting the central banking system.

This is especially pertinent for Bitcoin, a unique asset that is both a store of value but could be made as a daily transaction driver. The question then poses itself, is a legalistic landscape viable in which low-value Bitcoin transactions are exempt from federal taxation?

Bitcoin’s Usage and Currency Substitution Suitability

To understand the regulatory path forward, we first need to understand how Bitcoin is typically used. After all, contrasting Bitcoin usage against fiat usage paints a clearer picture if Bitcoin can be used as a practical currency, or if it will be perceived as a threat to the current monetary system.

Notwithstanding layer 2 scaling solutions such as Lightning Network, the more BTC is used the greater is the load on the Bitcoin mainnet as miners process transaction blocks. In turn, greater network activity generates greater friction, manifesting as escalating fees for each BTC transaction.

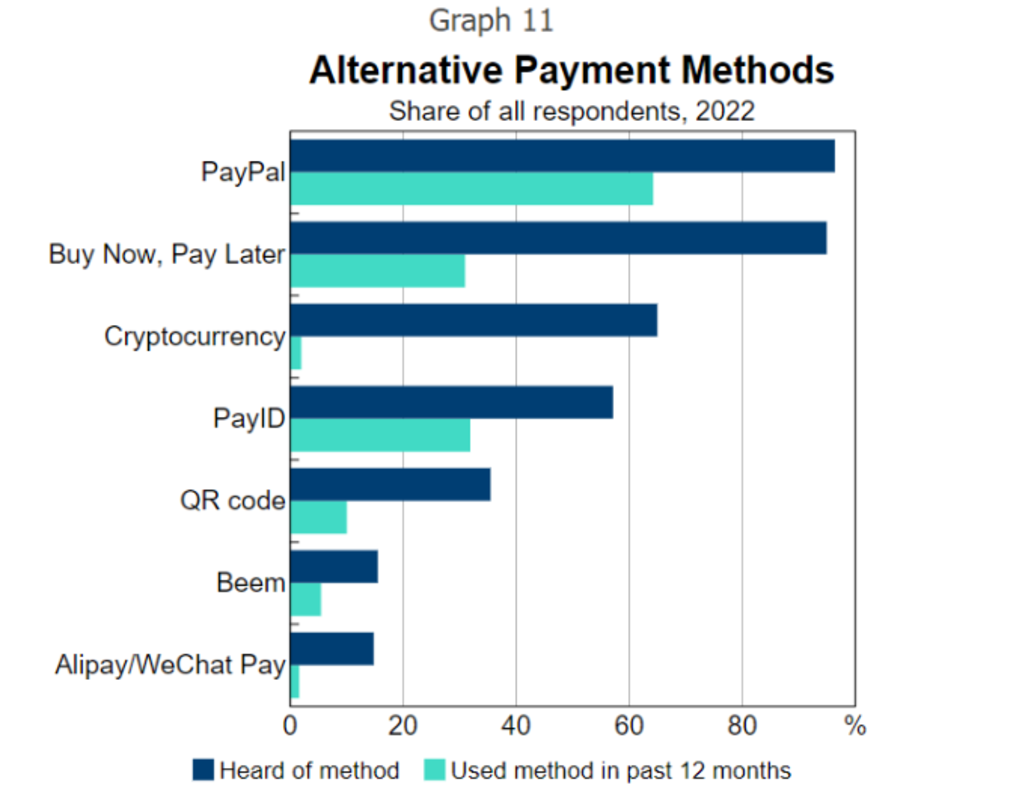

In a developed country like Australia, cryptocurrency usage for payments has been typically minimal.

Image credit: Reserve Bank of Australia

This is predictable as people need strong incentives to move away from existing payment solutions, ones that are already instantaneous and convenient.

At best, BTC transactions mostly revolve around third-parties facilitating BTC transactions using fiat currency. Case in point, Bitcoin onramp platform Strike had to ditch Prime Trust custodian as it eventually filed for bankruptcy. However, Strike still uses banks such as Lead, Cross River Bank, and Customers Bank.

In other words, Bitcoin adoption is attached to online payment systems, through commercial banks which are tied to central banks. The latter have already made money de facto digital, except it is hosted on their ledgers.

Although these institutions can tamper with the money supply, they can do so to facilitate maximum liquidity needed for a debt-based monetary system in which fiat currency is effectively a debt-tracker.

In contrast, Bitcoin’s scarcity makes it less appealing for such use. Gold already showcased this when it was abandoned. Because gold’s supply was not flexible enough to support a growing (debt-based) economy, mainstream economists viewed the gold-backed currency as outdated.

Moreover, Bitcoin is ill-suited as a daily currency driver against feeless alternatives like Nano (XNO) that boast eco-friendly green hosting or potential CBDCs. Rather, Bitcoin’s strength relies on inviolable scarcity, one that serves as a global reserve settlement layer.

While both of these factors, network friction and flexible liquidity, are making Bitcoin less suitable as a proper medium of exchange, it also makes Bitcoin less threatening to the system. But does that mean that Bitcoin’s tax treatment should be tweaked?

The Impact of Current Tax Policies on Bitcoin Usage

On exchanges and platforms like aforementioned Strike, users can freely buy Bitcoin without worrying it will be a taxable event. It only becomes so when BTC is sold for profit. Then, it is subject to capital gains tax for trading.

That’s because the Internal Revenue Service (IRS) designates Bitcoin as property. If Bitcoin is held less than a year before it is sold, holders are subject to ordinary income tax rate ranging from 10% to 37%.

Holding Bitcoin over one year makes it subject to 0% – 20% tax rate, depending on the income level spread across three brackets – 0%, 15% and 20%. In turn, Bitcoin holders have to keep a track of when they bought BTC, at which price, and when they sold it, at which price. The profit difference is taxed as capital gains.

Likewise, swapping Bitcoin for another cryptocurrency is a taxable event, subject to capital gains tax. If BTC is received as payment/earnings, or from mining/staking/airdrops, it is then treated as wages income tax, falling into the 10% – 37% ordinary income tax range.

Alongside buying BTC, holding it or donating it to a registered non-profit, users can also transfer bitcoins from exchanges to wallets without constituting taxable events. Although BTC gifts can also pass as non-taxable upon reception, they would still be subject to the same tax regime later.

In the case of selling Bitcoin at a loss, holders could write it off, limited to $3,000 per year (carriable into next year if exceeded). At the moment, it is still possible to engage in Bitcoin tax-loss harvesting, in which holders can sell BTC at a loss to claim the tax break, and then buy it back.

Unfortunately, this leeway not enjoyed by shareholders could be terminated with the proposed Lummis-Gillibrand Responsible Financial Innovation Act, under Section 1091, “Loss from wash sales of specified assets”.

But even with that tax break still open, it is clear that Bitcoin’s unique nature is not reflected in IRS treatment. The tracking alone of every BTC transaction severely discourages daily use as the mere purchase of a pint of beer would require calculating initial BTC price to see whether it was at a loss or at a gain.

Likewise, merchants would have to hassle with the same tax regime because they technically received property, not money. Combined with the previously mentioned issues of friction and flexible liquidity, this puts an additional burden on mass Bitcoin adoption by incentivizing long-term holding.

Moreover, Bitcoin’s expansion into innovative financial products is impeded as well.

The Tax Burden on Bitcoin Derivatives

Although Bitcoin has become the least volatile cryptocurrency due to its large $1.2 trillion market cap, holders would still prefer to protect themselves against price fluctuations. Derivatives, such as options and futures, make this possible.

Additionally, Bitcoin’s price volatility creates opportunities for traders willing to bet if BTC price will go up (going long) or down (going short). This speculative market important for risk hedging and price discovery is also burdened by the current tax regime.

Once an options contract is exercised, or when it expires, it is subject to capital gains tax. Most traders will create trading alerts to signal the moment BTC price crosses a certain threshold. This helps traders to respond quickly as the loss or capital gain tax is calculated based on the difference between Bitcoin’s fair market value and the strike price. So, staying consistently updated on Bitcoin’s fair market value is a challenge.

Additional difficulty would be to calculate the fair market of another cryptocurrency if it was the vehicle for Bitcoin contract settlement.

But if the contract expires without buying BTC, the capital loss would be regarded as the paid premium for the contract. On the other end of the equation, sellers of Bitcoin options premiums would have to pay capital gains tax as well.

When it comes to futures contracts, 60% of gains/losses are taxed as long-term capital gains/losses, while 40% are taxed as short term capital gains/losses. This is irrespective of futures contract length.

While derivatives markets greatly enhance liquidity and trading volume, the current Bitcoin tax regime discourages broader participation.

The Virtual Currency Tax Fairness Act and Bitcoin

The year 2024 turned into a massive pileup of good news for Bitcoin, barely bothered by the German government’s BTC selloffs. The most recognizable cryptocurrency received an institutional blessing when the Securities and Commissions Exchange (SEC) approved 11 exchange-traded funds (ETFs), having climbed to $48.13 billion AuM as of August 20th.

Not only did Bitcoin ETFs exceed all expectations, but their success served as an endorsement ramp for two presidential candidates, Robert F. Kennedy Jr. and former President Donald Trump. Both endorsed the idea of a strategic Bitcoin reserve at the Nashville Bitcoin 2024 conference at the end of July.

Just at that time, senators Ted Budd (R-NC), Krysten Sinema (I-AZ), Cynthia Lummis ( R-WY) and Kirsten Gilibrand (D-NY) re-introduced bill S.4808, the Virtual Currency Tax Fairness Act.

As the bill’s title implies, cryptocurrencies would receive the same tax treatment that is currently reserved for foreign currencies.

Meaning, under the value of $200, cryptocurrency transactions would only be subject to regular sales tax. Although this is still behind El Salvador’s approach of having Bitcoin as legal tender, the bill would immediately lift the barrier for small item purchases in merchant locations.

Previously, one of the co-sponsors, Sen. Cynthia Lummis, noted she is “absolutely certain that Bitcoin will be among them…and perhaps dominant among them”, referring to a future world order based on a basket of global reserve currencies.

As of the latest campaign development, presidential candidate Kamala Harris is in favor of President Biden’s 44.6% capital gains tax, in addition to raising the corporate tax rate from 21% to 28%.

The Broader Implications for Bitcoin Adoption

Although to a lesser extent, recession is still on the table moving into 2025. If materialized, this will be another BTC price test, if its risk-off status will be light or heavy. But on the long-term horizon, the structure of mass democracy doesn’t allow for austerity.

And if austerity is not on the horizon, the ballooning of the Fed’s balance sheet is, inevitably eroding USD confidence. It is anyone’s guess if factions vying for power will allow Bitcoin to become a potential exit vehicle on that road.

Making BTC transactions under $200 subject to sales tax, instead of capital gains tax, would go a long way in further ingraining Bitcoin into the financial system. Considering that Blackrock’s IBIT has become the largest Bitcoin ETF, at $17.24B AuM, it is fair to say that Bitcoin’s “threat” perception has been muted, if not abandoned.

Conclusion

Currently priced at above $60k per BTC, it is becoming increasingly clear that only a tiny micro minority will ever own more than 1 BTC. Accordingly, such a small population pool is unlikely to shake the proverbial central banking boat.

What is more likely to form is a parallel, hybrid system in which Bitcoin is both a commodity and a premium currency that is tracked. This is evidenced by the fact that even senators not explicitly anti-crypto want expansive cryptocurrency surveillance.

And Bitcoin’s transparent ledger is ideally suited for it. This is a positive development as privacy-oriented cryptocurrencies like Monero (XMR) have already been ousted from the largest exchange onramps.

Without those headwinds when sailing on a fiat ocean, Bitcoin is free to foster greater financial inclusivity and innovation despite the onramp/offramp barriers, including taxing an appreciating asset. The Virtual Currency Tax Fairness Act is paving the road, but it is likely to receive more tweaks. Specifically, it is yet not clear how transactions amounting to $200 are aggregated.

This is a guest post by Shane Neagle. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.